Short update for Q1 2016, ending June 30, 2015

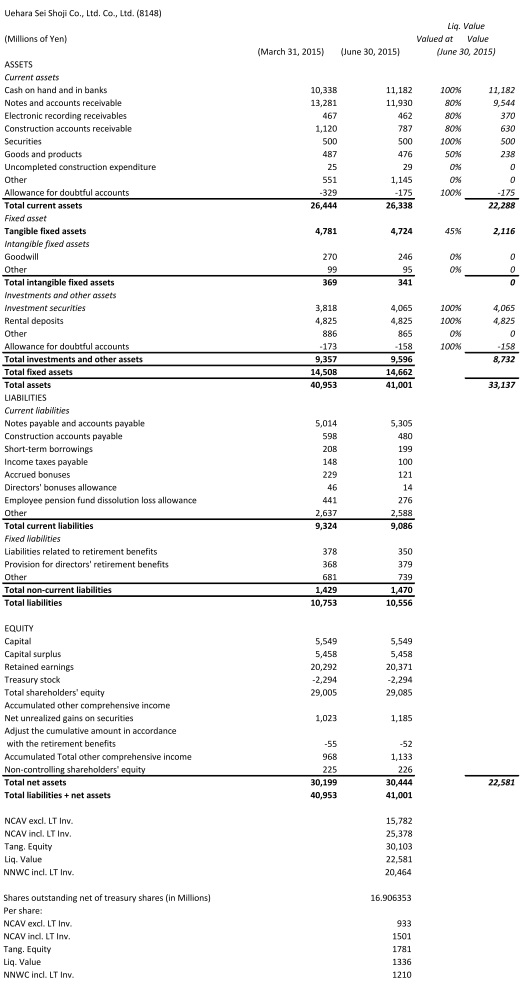

Uehara Sei Shoji Co disclosed results for the first quarter of FY 2016 today. The company made a net profit per share of ¥9.02. The “liquidation value” has hardly changed at all:

(Source: Quarterly report for the first quarter of FY 2016)

The company didn’t disclose the individual tangible assets accounts. I therefore used the weighted average multiplier for tangible assets from the liquidation analysis for the last quarter. The difference in this account is negligible. I included one additional variable:

NNWC incl. LT Inv. : = Cash + 0.8 Accounts receivable + ST Securities + 0.5 Inventory – Allowance for doubtful accounts + Investment securities + Deposits – Total liabilities.

I encountered some investors, who found it inappropriate to deduct treasury shares from what the company reports as “shares outstanding”. They argued that as long as treasury stock isn’t retired, the share count does not decline. While it is technically true that the share count does not decline if the shares are not retired, holding treasury stock is economically equivalent to retiring bought back stock. In calculating EPS, the company does rightfully deduct treasury stock from “outstanding shares”. Some of the confusion might stem from the fact that outstanding shares is generally defined as issued shares minus treasury shares. Japanese corporations, however, report outstanding shares inclusive of treasury shares. It might be a translation mistake. However, the likelihood for that is very low as I tried many languages and in all cases it is translated as “outstanding shares”. This, in general, presents an opportunity as many databases naïvely calculate the market capitalization using “outstanding shares”. As many Japanese corporations own treasury shares, the market capitalization, and therefore the valuation, is overstated for many Japanese stocks.

Disclosure: The author is long 8148:Tokyo.