Profitable Japanese net-net, share buyback, increasing net current asset value per share, inaccurate database numbers, small, off the beaten path

Uehara Sei Shoji is a Japanese net-net. At the current market price of ¥519 per share, it trades at a 65% discount to its net current asset value of ¥1,481/share (including long-term investments, which consist mostly of investment securities and rental deposits). Tangible equity per share is ¥1,764. This equates to a P/Tang. B of 0.29. Management has consistently been buying back stock. As of March 31, 2015, Uehara owns 7,147K of the total of 24,053K issued shares. Hence, there are 16,906K shares outstanding net of treasury stock. So Uehara owns roughly 30% of its own shares! This might be a contributing reason for its very cheap valuation, as many databases provide an inaccurate market capitalization number. As a consequence, a superficial screen would overestimate the valuation. With an actual market cap. of ¥8.774 billion (= US$71 million) Uehara is too small for larger investors. Financial reports are only available in Japanese, which should render the stock “uninvestable” for many individual investors outside Japan. Graham/Dodd investing appears to be not prominent among Japanese individual investors. Together, this might contribute to a deep neglect of the stock. The downside is sufficiently protected by a cash balance of ¥9,936 (cash ¥10,338 – debt and capital leases ¥402) and a history of profitability. Buying back shares at these low prices is hugely value accretive.

“Uehara Sei Shoji Co., Ltd. operates as a trading company in Japan. It sells construction materials, and products for energy, housing, and other facilities. The company’s products include cement, ready-mixed concrete, sash, glass, pile, lightweight external wall material, housing equipment, other building materials, gasoline, light and heavy oil, lubricant, propane gas, butane gas, and compressed natural gas, as well as car maintenance products. Uehara Sei Shoji Co., Ltd. was founded in 1943 and is headquartered in Kyoto, Japan.” (Source: Bloomberg)

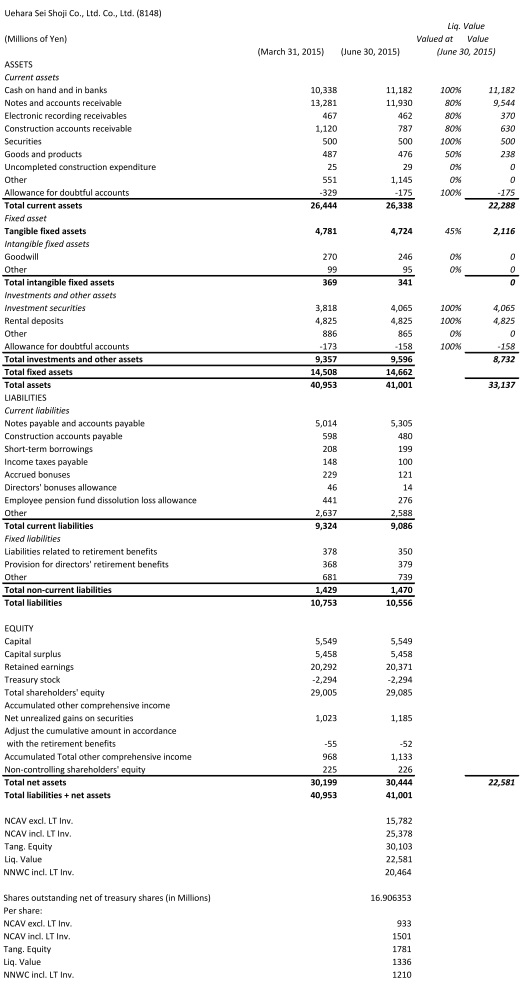

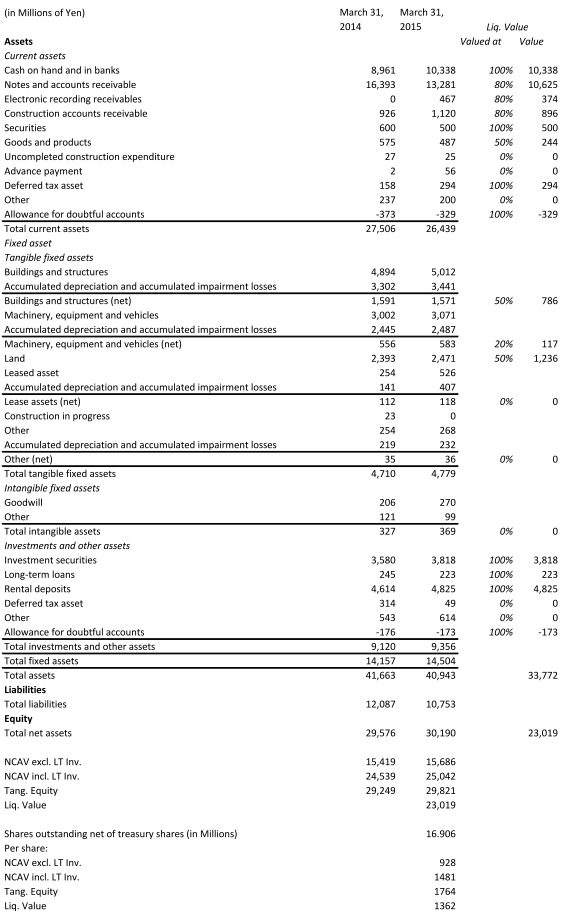

The Company has been consistently profitable over the last 10 years. In FY2015 Uehara made a net profit of ¥547 Million. Management guides to a net profit of ¥550 million in FY2016. This means the company generates only a 1.8% return on tangible equity. This is due to large cash holdings and holdings of securities, which is quite typical for Japanese corporations. The enterprise value is negative. (Or positive but very small if factors in that some cash is needed for the operations). Earnings, however, are secondary to the thesis. This is an asset play. The “liquidation value” is considerably higher than the price. I don’t expect the company to liquidate any time soon. However, a company that isn’t burning through its cash should not trade at such a low valuation. Below is the translated balance sheet from the annual report of FY 2015 (using Google Translate) and a calculation of the approximate liquidation value:

(Source: Annual Report 2015)

As mentioned before the company has bought back very large amounts of shares. And, most importantly, they have been bought at great prices. I tabulated the share count (in thousands) over the last 11 years below:

(Source: Annual Report 2006 – 2015)

Taking cash out of the bank account and buying your own cash at a discount plus all other net assets for free is a no-brainer. By taking this action, Management has been acting very shareholder friendly. The Uehara Family is the largest holder with 1,640K shares (Source: FactSet), which represent 9.7% of the outstanding shares net of treasury stock. Thus, management’s interest should be aligned with minority shareholders’.

This is not a high conviction idea. I cannot read a word in Japanese. All information has been gathered from filings by the company using Google Translate. I might be missing something important. The stock only represents a small position in my diversified net-net portfolio. However, with the large buyback, the company acts vastly more shareholder friendly than many other Japanese net-nets. If this behavior continues, it should also serve as a catalyst for closing the valuation gap. The downside is very limited and the upside should be between “liquidation value” of roughly ¥1360/share and tangible equity of ¥1760/share.

Disclosure: The author is long 8148:Tokyo.