On Friday 10/23/2015 Art Vivant announced a favorable outcome of a legal dispute. In response, management raised the profit guidance and declared special dividends. I took advantage of the subsequent surge in the stock price and sold my position for a +56% gain in two months.

STR Holdings Inc (STRI:OTC)

- Delisting resulted in indiscriminate selling

- >400% upside to private market value

- >250% upside to NCAV (which is likely to increase due to liquidation of Malaysian facility)

- Limited downside due to 72% discount to NCAV and no debt

- History of shareholder friendly actions

- Reasonable probability of returning to profitability due to synergies with new controlling shareholder and cost cutting initiatives

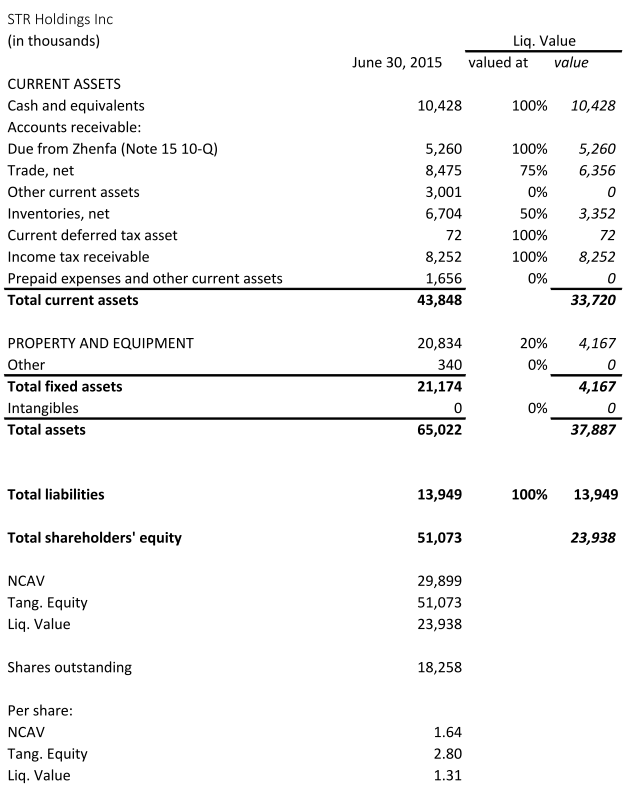

STRI was delisted from the NYSE on September 29, 2015 “[…] due to its failure to maintain an average global market capitalization over a consecutive 30 trading-day period of at least $15 million.” Since 09/30/15 it trades OTC. I think the stock price crashed on this day due to indiscriminate selling. On 09/29/15 STRI closed at $0.79. The price subsequently reached a low of $0.37 on 09/30/15, a more than 50% decline in one day without any other news and no change in reporting obligations with the SEC.[1] The price has recovered since then to $0.46 on 10/03/15 but the stock is still one of the cheapest net-nets around. At a discount of 72% to NCAV and an above net-net-average quality of the business, STRI is one of the most attractive opportunities at the time.

STRI supplies Ethylene Vinyl Acetate encapsulants to the photovoltaic module industry. I’m not an expert in the solar industry and will not attempt to judge the longer-term viability of STRI’s products and its market position. It appears, however, that STRI is a leading supplier as the company caters to well-known solar companies. I think solar power will be the number one source of energy long-term. However, I will not give this information any weight in valuing this company. This is the same problem an investor faced at the inception of the auto industry, airline industry or the internet. It is one thing to forecast the impact of an industry on society. It is a whole different story to pick the winners and/or project the distribution of earnings and losses.

On 12/15/14 STRI announced that Zhenfa Energy Group purchased 27.6 million newly issued shares of common stock (before the reverse-split), representing a 51% interest in STRI for $21.7 million. [2] STRI’s CEO states: “As one of the top solar engineering, procurement and construction companies in China, and a leading solar independent power producer as well, Zhenfa is ideally positioned to directly benefit from the use of STR’s market-leading encapsulant technology and also to advocate its use to Chinese module manufacturers. Zhenfa’s substantial investment reflects their confidence in STR’s ability to become profitable and grow in the rapidly expanding solar industry.”[3] This transaction price can be seen as an indication of intrinsic value as defined by the price a strategic buyer would pay for the business. On 01/02/15 STRI paid out a special dividend of $2.55 per share other than Zhenfa’s shares. On 02/02/15 STRI carried out a 1:3 reverse split. By buying 51% of the company (without the right to receive the special dividend) for $21.7 million, Zhenfa effectively valued the whole business in excess of $42.5 million 10 month ago. At today’s share count of ~18 million, this represents a private market value of ~$2.36/share. Since the closing of the transaction, STRI incurred further losses. These were probably expected by Zhenfa and thus don’t impair the $2.36/share purchase price, which seems reasonable in comparison to the tangible book value of $2.8/share. At the closing price on Friday of $0.46, this translates into an upside of over 400%. Further, STRI plans to close its Malaysian facility in response to its largest customer ceasing operations in Malaysia. Management expects $8 million proceeds from the sale of real estate and $1 million to $1.5 million one-time costs mainly due to severance payments partially offset by proceeds from the sale of equipment. If the liquidation turns out as expected, this would increase my estimate of liquidation value (and NCAV) substantially. In addition, the closure of this facility is expected to improve the utilization of STRI’s other facilities and thus will probably benefit profitability.

(Source: 10-Q for the Second Quarter Ending June 30, 2015)

Despite the recent unprofitability, I think STRI has been acting very shareholder friendly. The company has a history of distributing special dividends, buying back stock and shrinking for the sake of shareholder value maximization. As the new controlling shareholder, Zhenfa is incentivized to maximize shareholder value by returning the company back to profitability. Despite the generally poor evidence of synergy manifestation, I think, in this case, the alliance really could be mutually advantageous. For this investment to be profitable for the minority shareholder, however, one doesn’t need the benefits of synergy. Just a return of the stock price to the current NCAV would render this investment very profitable. Since the transaction, one director bought ~$90k worth of stock between $1.11 and $1.13.[4] Lloyd Miller III also has a position in STRI. His name appears frequently in the ownership tables of net-nets and in case of shareholder abuse, he assumes the role of an activist investor.

In summary STRI is an unusually attractive net-net. The company is a leader in its niche. The price is probably depressed due to price insensitive selling in response to the recent delisting. The downside is protected by current assets, especially the large net cash balance (no debt), which is likely to increase substantially due to the liquidation of the Malaysian facility. Historically, the company has been shareholder friendly by distributing excess cash to shareholders in the form of special dividends and share buy-backs. There is a reasonable probability of the company to return to profitability due to synergies and cost cutting. The private market value is around $2.36/share (>400% upside). NCAV is around $1.64/share and will probably increase due to the aforementioned liquidation. This situation combines a very large upside potential and limited downside AND an above average probability of a favorable outcome.

Disclosure: The author is long STRI.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

[1] See: Form 8-K (September 29, 2015), p. 2.

[2] See: Announcement by the Company (December 15, 2014)

[3] See: Announcement by the Company (December 15, 2014)

[4] See: Form 4 (May 18, 2015)

Art Vivant Co Ltd (7523:Tokyo)

Profitable net-net, inaccurate database numbers, small market cap

Art Vivant operates in art related businesses. The business model is however quite diffuse. According to the Japan Company Handbook, the company is a top ranked seller of modern lithography art and other artworks. The company targets customers in the range between 20 and 30 years old. The company is also engaged in the operation of fitness clubs, yoga studios, an app called “Wonder4World” and a hotel under the name “Tarasa Shima Hotel and Resort”. Art Vivant also provides financial services with artworks as collateral.

Management guides to a net profit of ¥510 million or ¥39 per share for FY 2016. Note that this information might be hard to find for foreign investors. This information, like the information regarding the shares outstanding, is on the first page of the quarterly report. For some reason, this page is formatted as a picture. Hence, an electronic translator like Google Translate will not translate this information. There is no way of knowing, by looking at the translated document, that this information is even there. The company reports in Japanese, only.

The company owns 2.387 Million treasury shares. This represents 15.44% of the 15.464 Million total issued shares. Thus, there are 13.077 million shares outstanding net of treasury shares. As I pointed out in the Uehara Sei Shoji Co write-up, many databases calculate an inaccurate market capitalization for Japanese companies as they don’t subtract treasury shares from issued shares. This is also the case for Art Vivant. Hence, superficial screens overestimate the market cap and, as a result, the valuation for Art Vivant. Based on the current market price of ¥344, the correct market cap is ¥4.499 billion (= $37.57 million). With such a small size, institutional investors are effectively excluded from investing in this company. The lack of institutional investors paired with inaccurate database numbers and hard to get financial information might result in the deep neglect of the stock.

Art Vivant trades at a 61% discount to its NCAV. If one includes investment securities and deposits in NCAV, the stock trades at a 63% discount. While the investment securities and deposits are technically non-current assets, it makes sense to include them in NCAV, I think, because of their liquidity.

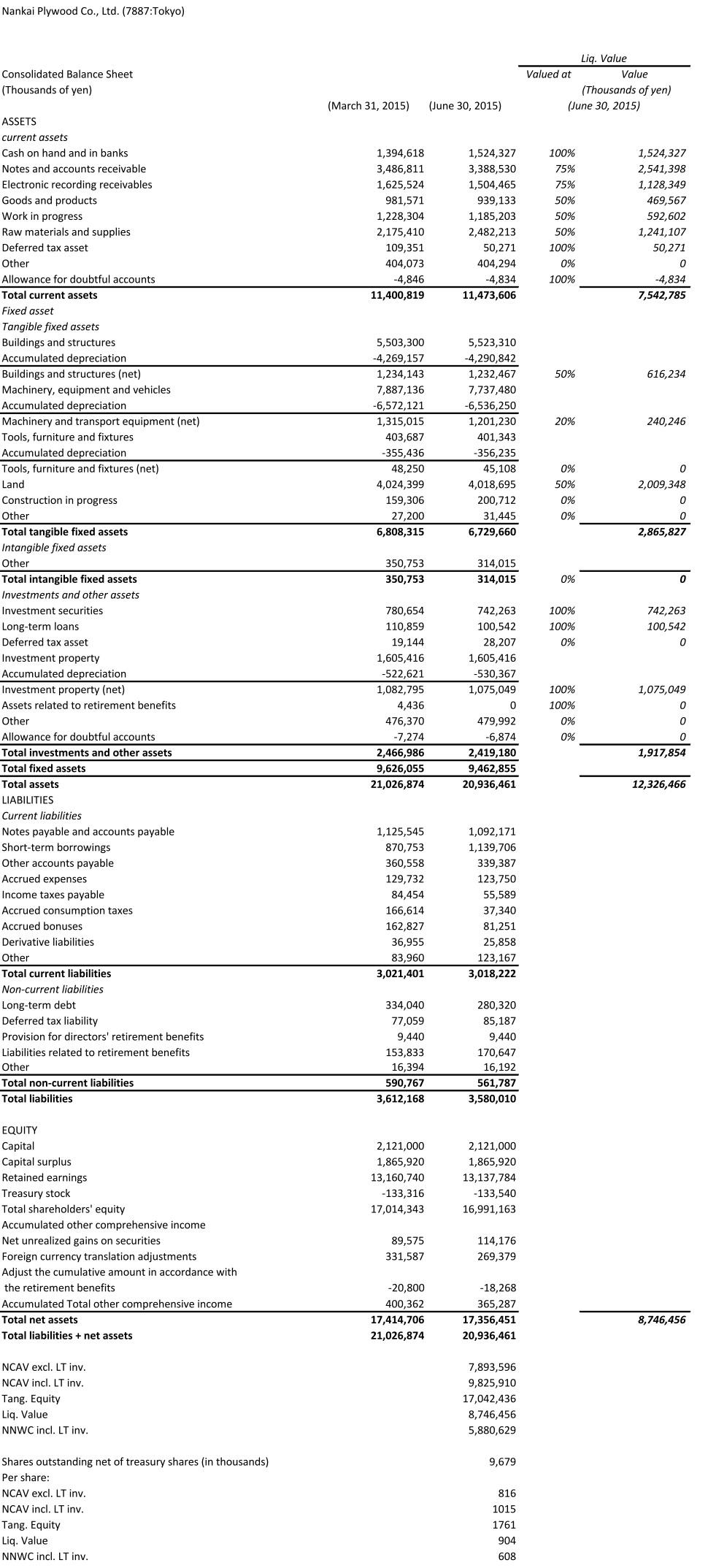

Below is the translated balance sheet (using Google Translate), the calculations of NCAV and an approximate liquidation value:

(Source: Quarterly report for the first quarter of FY 2016)

Disclaimer: This stock represents only a small percentage of my net-net basket. Stocks in this basket are picked based on quantitative variables. Almost no qualitative analysis is performed for these statistical picks.

Disclosure: The author is long 7523:Tokyo.

Nankai Plywood Co Ltd (7887:Tokyo)

Japanese net-net

Nankai Plywood Co. is another Japanese net-net. Earnings over the last 10 years have been volatile but, on average, positive. Management guides to a net profit of ¥15.50 per share for the FY 2016. According to the Japanese Company Handbook, the company is a top ranked manufacturer of Japanese-style room ceilings and floors, holding the highest market share in laminated ceilings. At its current market price of ¥412 per shares, it’s trading at a market cap of ¥3.988 billion (= US$32.034 million). With such a small market cap, institutional investors are effectively excluded from participating. It trades at a 49% discount to its NCAV of ¥7.894 billion. If one includes long-term investments in NCAV – which is sensible, I think, if one views NCAV as a proxy for liquidation value – it trades at a 59% discount. The company also owns a substantial amount of tangible fixed assets. Especially land, which I conservatively valued at 50% of book value in the liquidation analysis, could be worth more. The P/Tang.B is very low at 0.23.

Below is the translated balance sheet (using Google Translate) and a liquidation value analysis:

(Source: Quarterly report for the first quarter of FY 2016)

Disclosure: The author is long 7887:Tokyo.

Uehara Sei Shoji Co Ltd (8148:Tokyo) Update

Short update for Q1 2016, ending June 30, 2015

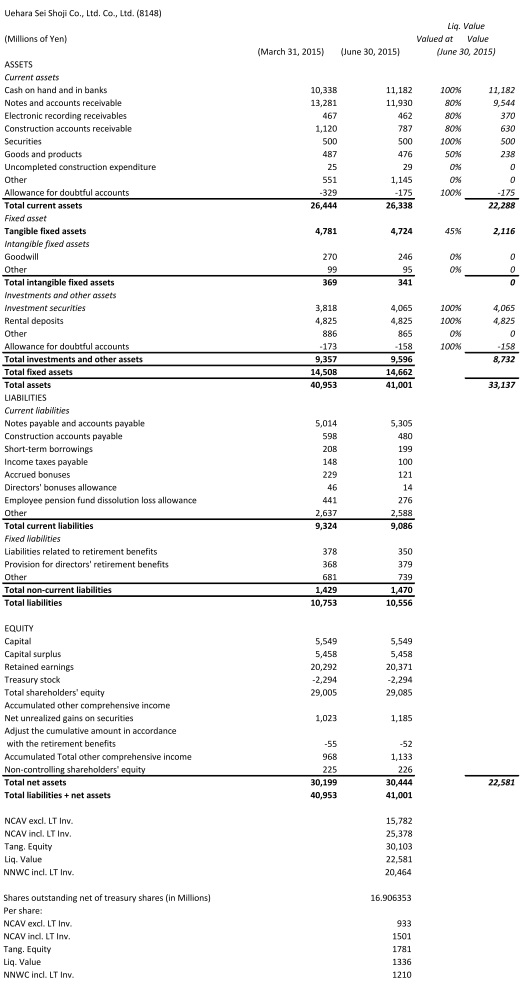

Uehara Sei Shoji Co disclosed results for the first quarter of FY 2016 today. The company made a net profit per share of ¥9.02. The “liquidation value” has hardly changed at all:

(Source: Quarterly report for the first quarter of FY 2016)

The company didn’t disclose the individual tangible assets accounts. I therefore used the weighted average multiplier for tangible assets from the liquidation analysis for the last quarter. The difference in this account is negligible. I included one additional variable:

NNWC incl. LT Inv. : = Cash + 0.8 Accounts receivable + ST Securities + 0.5 Inventory – Allowance for doubtful accounts + Investment securities + Deposits – Total liabilities.

I encountered some investors, who found it inappropriate to deduct treasury shares from what the company reports as “shares outstanding”. They argued that as long as treasury stock isn’t retired, the share count does not decline. While it is technically true that the share count does not decline if the shares are not retired, holding treasury stock is economically equivalent to retiring bought back stock. In calculating EPS, the company does rightfully deduct treasury stock from “outstanding shares”. Some of the confusion might stem from the fact that outstanding shares is generally defined as issued shares minus treasury shares. Japanese corporations, however, report outstanding shares inclusive of treasury shares. It might be a translation mistake. However, the likelihood for that is very low as I tried many languages and in all cases it is translated as “outstanding shares”. This, in general, presents an opportunity as many databases naïvely calculate the market capitalization using “outstanding shares”. As many Japanese corporations own treasury shares, the market capitalization, and therefore the valuation, is overstated for many Japanese stocks.

Disclosure: The author is long 8148:Tokyo.

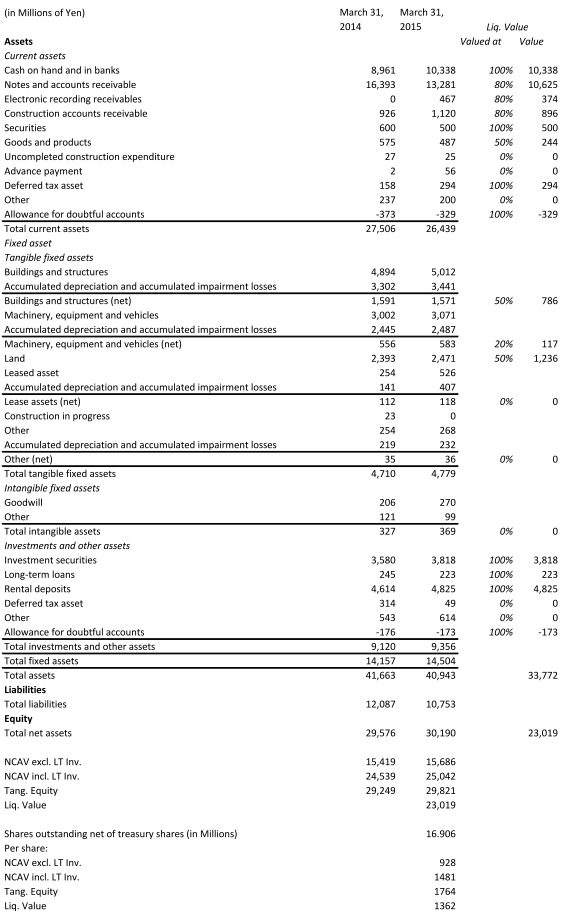

Uehara Sei Shoji Co Ltd (8148:Tokyo)

Profitable Japanese net-net, share buyback, increasing net current asset value per share, inaccurate database numbers, small, off the beaten path

Uehara Sei Shoji is a Japanese net-net. At the current market price of ¥519 per share, it trades at a 65% discount to its net current asset value of ¥1,481/share (including long-term investments, which consist mostly of investment securities and rental deposits). Tangible equity per share is ¥1,764. This equates to a P/Tang. B of 0.29. Management has consistently been buying back stock. As of March 31, 2015, Uehara owns 7,147K of the total of 24,053K issued shares. Hence, there are 16,906K shares outstanding net of treasury stock. So Uehara owns roughly 30% of its own shares! This might be a contributing reason for its very cheap valuation, as many databases provide an inaccurate market capitalization number. As a consequence, a superficial screen would overestimate the valuation. With an actual market cap. of ¥8.774 billion (= US$71 million) Uehara is too small for larger investors. Financial reports are only available in Japanese, which should render the stock “uninvestable” for many individual investors outside Japan. Graham/Dodd investing appears to be not prominent among Japanese individual investors. Together, this might contribute to a deep neglect of the stock. The downside is sufficiently protected by a cash balance of ¥9,936 (cash ¥10,338 – debt and capital leases ¥402) and a history of profitability. Buying back shares at these low prices is hugely value accretive.

“Uehara Sei Shoji Co., Ltd. operates as a trading company in Japan. It sells construction materials, and products for energy, housing, and other facilities. The company’s products include cement, ready-mixed concrete, sash, glass, pile, lightweight external wall material, housing equipment, other building materials, gasoline, light and heavy oil, lubricant, propane gas, butane gas, and compressed natural gas, as well as car maintenance products. Uehara Sei Shoji Co., Ltd. was founded in 1943 and is headquartered in Kyoto, Japan.” (Source: Bloomberg)

The Company has been consistently profitable over the last 10 years. In FY2015 Uehara made a net profit of ¥547 Million. Management guides to a net profit of ¥550 million in FY2016. This means the company generates only a 1.8% return on tangible equity. This is due to large cash holdings and holdings of securities, which is quite typical for Japanese corporations. The enterprise value is negative. (Or positive but very small if factors in that some cash is needed for the operations). Earnings, however, are secondary to the thesis. This is an asset play. The “liquidation value” is considerably higher than the price. I don’t expect the company to liquidate any time soon. However, a company that isn’t burning through its cash should not trade at such a low valuation. Below is the translated balance sheet from the annual report of FY 2015 (using Google Translate) and a calculation of the approximate liquidation value:

(Source: Annual Report 2015)

As mentioned before the company has bought back very large amounts of shares. And, most importantly, they have been bought at great prices. I tabulated the share count (in thousands) over the last 11 years below:

(Source: Annual Report 2006 – 2015)

Taking cash out of the bank account and buying your own cash at a discount plus all other net assets for free is a no-brainer. By taking this action, Management has been acting very shareholder friendly. The Uehara Family is the largest holder with 1,640K shares (Source: FactSet), which represent 9.7% of the outstanding shares net of treasury stock. Thus, management’s interest should be aligned with minority shareholders’.

This is not a high conviction idea. I cannot read a word in Japanese. All information has been gathered from filings by the company using Google Translate. I might be missing something important. The stock only represents a small position in my diversified net-net portfolio. However, with the large buyback, the company acts vastly more shareholder friendly than many other Japanese net-nets. If this behavior continues, it should also serve as a catalyst for closing the valuation gap. The downside is very limited and the upside should be between “liquidation value” of roughly ¥1360/share and tangible equity of ¥1760/share.

Disclosure: The author is long 8148:Tokyo.